Understanding Medicare Supplements : A Comprehensive Guide

#Understanding Medicare Supplements: A Comprehensive Guide

Navigating the world of Medicare can be overwhelming, especially when it comes to understanding Medicare supplements, also known as Medigap policies. These plans are essential for covering costs that original Medicare doesn’t fully pay for, like copayments, coinsurance, and deductibles. This comprehensive guide will walk you through the basics of Medicare supplements, how they work, and why you might consider them.

What Are

What Are Medicare Supplements ?

How Do Medicare Supplements Work?

What Do Medicare Supplements Cover?

- Copayments: A fixed amount you pay for a covered health service.

- Coinsurance: Your share of the costs of a covered healthcare service, calculated as a percentage.

- Deductibles: The amount you pay for healthcare services before your insurance begins to pay.

Different

Types of Medicare Supplement Plans

In the United States, there are ten standardized

Plan A

Plan A

Plan A offers the basic benefits of

Plan F

Plan F is one of the most comprehensive

Plan G

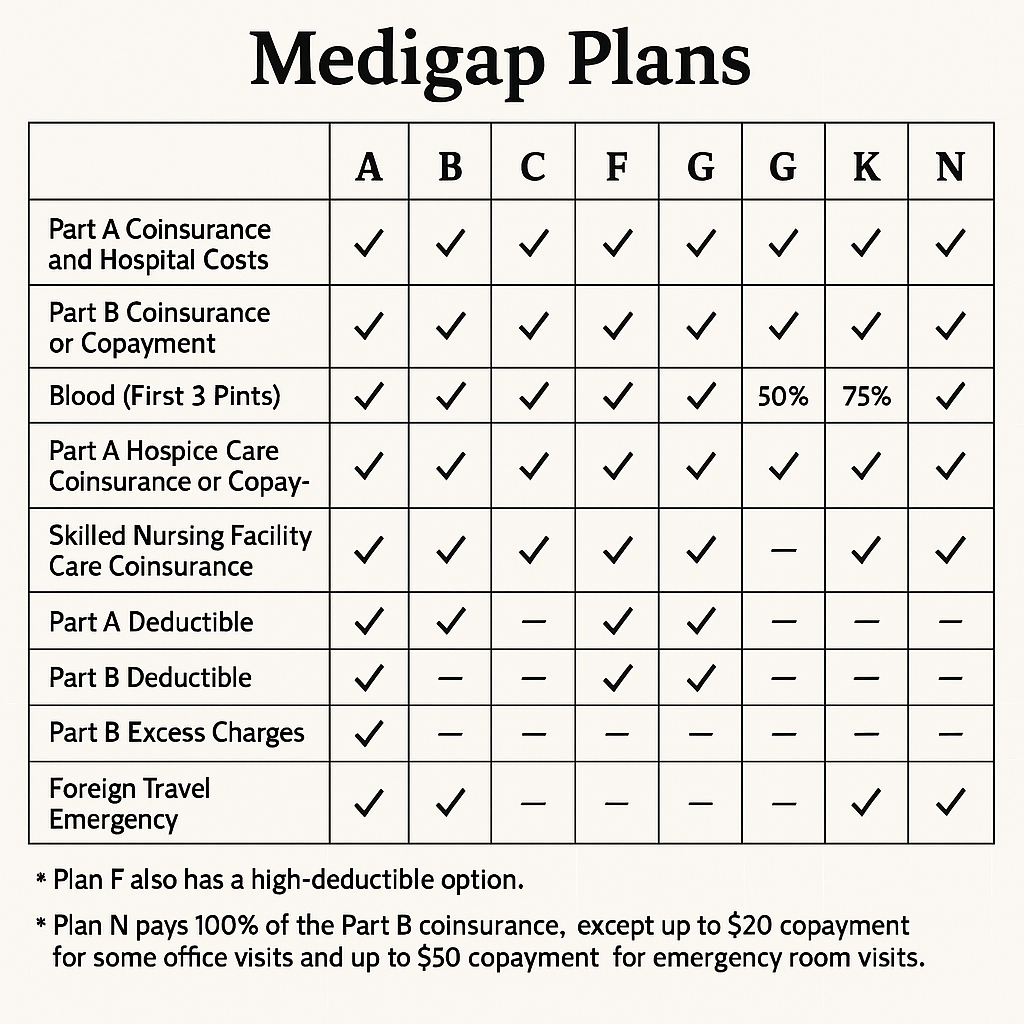

Plan G is similar to Plan F but does not cover the Medicare Part B deductible. It is often considered the best option for new Medicare beneficiaries because it offers comprehensive coverage.

Plan N

Plan N covers the same benefits as Plan G, except that you are responsible for a copayment of up to $20 for some doctor visits and $50 for emergency room visits that do not result in inpatient admission.

Choosing the Right Medicare Supplement Plan

Choosing the right

Budget and Costs

Consider how much you can afford to pay in monthly premiums, as well as any out-of-pocket costs you might incur. While some plans might have higher premiums, they may offer lower out-of-pocket costs.

Healthcare Needs

Evaluate your current healthcare needs and anticipate any future needs. If you have frequent doctor visits or require specialist care, you might benefit from a more comprehensive plan.

Eligibility and Enrollment

You must have Medicare Part A and Part B to purchase a

How to Enroll in a Medicare Supplement Plan

Enrolling in a

- Research and Compare Plans: Use online tools or consult with a licensed insurance agent to compare different

Medigap plans and find the right one for you. - Contact Insurance Companies: Once you’ve identified a suitable plan, contact the insurance companies offering it to get quotes and confirm the details of the coverage.

- Enroll in the Plan: Complete the application process with the insurance company of your choice. Ensure you understand the terms and conditions before finalizing your enrollment.

Frequently Asked Questions

Can I Switch Medigap Plans?

Yes, you can switch

Are Prescription Drugs Covered by Medigap ?

No,

Can I Have a Medicare Advantage Plan and a Medigap Policy?

No, you cannot have both a Medicare Advantage Plan and a

Conclusion

Understanding

Featured Blogs

- ER, Urgent Care, or Virtual Visit? Where to Go and What It’ll Cost You

- Walk First, Wander Later: The Travel Hack You’ll Wish You’d Known Sooner

- Key Man Insurance Explained: Coverage, Structure, and Tax Implications

- Understanding Term Life Insurance Convertibility: Your Future Self May Thank You

- Rip Tides: What They Are, How to Spot Them, and What to Do If You're Caught in One

- The Benefits of Visiting Your Farmers Market this Summer

- Concierge Medical Care: A New Way To Better Health

- Safe Travels: How to Prepare Your Family for an International Vacation

- Ocean, Lakes, and Pools, Oh My! Tips for a Safe Summer Around Water

- Understanding the EOB: What Is It and Why Should You Care?

- Why Your Dentist Might Be Your Most Important Healthcare Provider

- Understanding the Unique Challenge

- Breathe Easy: The Surprising Benefits of Houseplants in Your Home

- Would You Bet $7,000 on Your Health This Year?

- When Life Happens: Building a Family Emergency Plan that Actually Works